- The New Fundraising Reality

- Limited Partners Raise the Bar

- Fundraising by Asset Class (2021–2025)

- The Rise of Sector-Specific Funds

- Operational Value as a Differentiator

- Secondaries and Continuation Funds as Tools of Differentiation

- The Investor's Perspective: Fewer Relationships, Deeper Conviction

- Conclusion: Differentiation as Destiny

Why 2025 Is the Year of Differentiation in Alternatives

The New Fundraising Reality

The fundraising climate in 2025 is marked by one word: selectivity. Investors are no longer chasing broad exposure to alternatives. Instead, they are concentrating capital into managers who demonstrate not only scale but also specialization, operational expertise, and the ability to deliver in an environment of higher rates and constrained liquidity.

While aggregate numbers show fundraising softness, the distribution tells a different story: a handful of differentiated managers are still raising large pools of capital, while many others are struggling to get off the ground.

Limited Partners Raise the Bar

Institutional investors, pensions, endowments, and sovereign wealth funds are adopting stricter criteria for commitments. Three key shifts stand out:

-

Track Record Over Brand: Investors are scrutinizing realized returns more than marketing narratives.

-

Sector Specialists Over Generalists: Funds with a sharp focus in AI infrastructure, energy transition, healthcare, or private credit niches are winning commitments.

-

Alignment and Transparency: Fee structures, GP commitment, and reporting clarity are central to LP diligence processes.

This environment rewards managers who can prove their edge and penalizes those leaning on reputation alone.

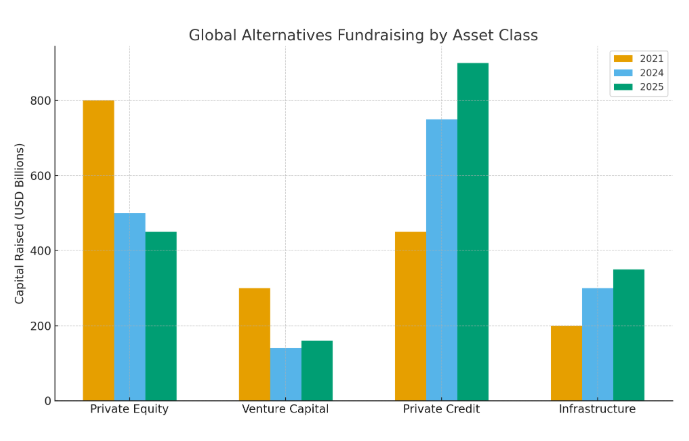

Fundraising by Asset Class (2021–2025)

Global fundraising trends highlight where capital is consolidating.

-

Private Credit has nearly doubled since 2021, surpassing $900 billion in 2025.

-

Venture Capital has fallen by almost half compared to its 2021 highs.

-

Infrastructure continues steady growth, crossing $350 billion in 2025.

-

Private Equity has slipped but remains the single largest pool.

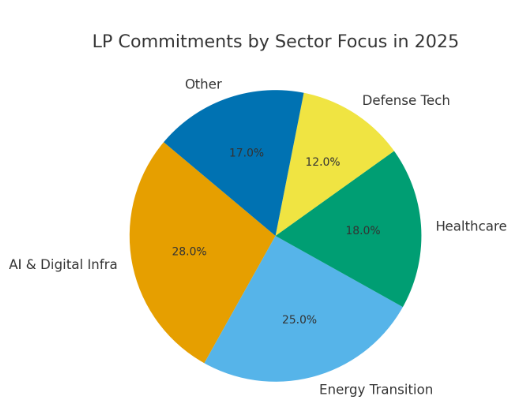

The Rise of Sector-Specific Funds

2025 has already seen outsized momentum in specialist vehicles:

-

AI and Digital Infrastructure: LP commitments have surged, with AI/data-related funds capturing nearly 28% of sector-focused capital this year.

-

Energy Transition: Driven by policy incentives, renewable and climate funds account for 25% of new allocations.

-

Healthcare & Life Sciences: Attracting 18% of targeted capital, buoyed by biotech recovery and demographic trends.

-

Defense Tech & National Security: A niche but fast-growing segment, pulling in 12% of sector-specific commitments.

The broader implication: the "index fund" approach to alternatives is fading, replaced by targeted exposure.

Operational Value as a Differentiator

In private equity, venture, and even private credit, value creation at the portfolio level is now the central narrative. With exit markets subdued, managers who can prove their ability to:

-

improve margins,

-

professionalize management teams,

-

digitize operations, and

-

scale efficiently

are being favored by LPs.

Secondaries and Continuation Funds as Tools of Differentiation

The secondaries market is now a $130 billion+ annual industry, with GPs increasingly deploying continuation funds to extend ownership of high-performing assets. Flexibility around liquidity has become a selling point for LPs wary of indefinite lock-ups.

The Investor's Perspective: Fewer Relationships, Deeper Conviction

Instead of maintaining dozens of GP relationships, large allocators are consolidating around fewer managers. This means:

-

larger ticket sizes for trusted GPs,

-

multi-strategy commitments to firms with proven diversification, and

-

a willingness to forgo smaller funds unless they provide a unique, defensible edge.

For LPs, 2025 is not about chasing every opportunity; it's about backing a select group of managers who can thrive in a tougher environment.

Conclusion: Differentiation as Destiny

2025 may be remembered as the year when the alternatives market shifted decisively from abundance to discernment. For managers, the challenge is clear: prove your edge, show operational value, and align tightly with investor priorities. For investors, the opportunity lies in concentrating capital where skill and strategy can still generate outperformance.

The age of easy fundraising is over. The age of selective capital and smarter managers has arrived.

Subscribe for updates

By providing your email, you agree to receive updates, onboarding information, and other communications related to accessing our platform.