From Mega-Funds to Modesty: Private Equity's Reset in 2025

Private Equity Fundraising in 2025: A Year of Pressure and Patience

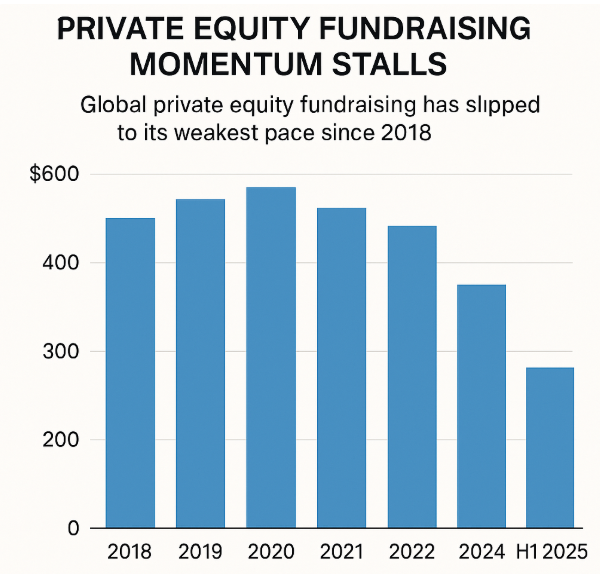

Private equity (PE) fundraising in 2025 has entered a challenging phase. While the appetite for alternative assets hasn't disappeared, global fundraising momentum is slowing, deal pipelines are clogged, and investors are signaling caution. Let's break down the trends shaping the industry at mid-year.

1. Fundraising Momentum Stalls

Global PE fundraising in H1 2025 reached just $247 billion, a 22% decline from the same period in 2024. More concerning: nearly 60% of that capital went to the top 20 managers.

The era of broad-based fundraising is over. LPs are doubling down on trusted names while shutting the door on emerging and mid-tier managers.

2. The Backlog Problem

The culprit behind sluggish fundraising? Unrealized value. PE portfolios are packed with companies acquired in 2020-2022 at peak valuations.

Exit activity has plummeted. IPO windows remain narrow, and strategic M&A is tepid. LPs are locked into funds that can't distribute cash, which in turn freezes their ability to commit to new funds.

It's a liquidity logjam—and it's forcing GPs to get creative with continuation vehicles, secondary sales, and recapitalizations just to keep the cycle moving.

3. No Mega-Funds, No Easy Wins

In the first half of 2025, only 3 funds crossed the $10 billion threshold. Compare that to 2021, when we saw double that number in the same period.

The mega-fund era, fueled by ZIRP and FOMO, is effectively on pause. LPs are tightening fund concentration policies, capping exposure to single managers, and scrutinizing fees more aggressively.

Even marquee names are facing longer fundraising cycles and more negotiations. The days of oversubscribed closes in under 6 months are behind us.

4. Venture Capital's Dimmed Hopes

While PE wrestles with exits, VC faces its own reckoning.

H1 2025 VC fundraising totaled just $38 billion globally—down 47% year-over-year. Late-stage funds have been hit hardest, with dry powder sitting idle as valuation resets continue.

Early-stage funds are still attracting commitments, but even seed managers are reporting longer closes and smaller fund sizes. The frothy optimism of 2021 has been replaced by sober due diligence and a flight to quality.

What This Means Going Forward

For the second half of 2025 and into 2026, expect:

- Longer fundraising cycles: 18-24 months will become standard, even for top-tier managers.

- Smaller fund sizes: GPs will rightsize targets to match realistic LP appetite.

- Portfolio focus over dealmaking: Expect more emphasis on operational improvements and strategic exits rather than new acquisitions.

- LP consolidation: Fewer, larger commitments to fewer managers. Middle-market and emerging managers will struggle.

- Secondary market growth: Both GP-led and LP-led secondaries will see record activity as liquidity becomes the primary concern.

Final Thought

2025 isn't a collapse—it's a reset. The PE and VC industries are recalibrating after a decade of exuberance. For investors, it's a return to fundamentals: discipline, selectivity, and patience.

The funds that survive this cycle won't be the flashiest. They'll be the ones that deliver real returns, manage portfolios actively, and earn their fees through performance—not PowerPoint.

Sources:

- Preqin Global Private Capital Report, H1 2025

- Pitchbook-NVCA Venture Monitor, Q2 2025

- Bain Global Private Equity Report, Mid-Year Update 2025

Subscribe for updates

By providing your email, you agree to receive updates, onboarding information, and other communications related to accessing our platform.